For more than a century, the paper check has been one of the most iconic tools in the American financial system. From paying rent to settling business invoices, checks shaped how Americans moved money long before digital banking existed. Yet in an era dominated by instant transfers and mobile payments, the paper check stands at a crossroads: still widely used, but undeniably fading. Understanding its history, its practical use, and its future helps explain why this seemingly old‑fashioned instrument remains surprisingly resilient in the United States.

A Brief History of the American Paper Check

The origins of the check trace back to ancient banking systems, but the American version began taking shape in the late 18th and early 19th centuries. As banks expanded across the young nation, checks became a convenient alternative to carrying large amounts of cash. By the early 1900s, checks were already a dominant payment method for businesses and households alike.

The golden age of checks arrived after World War II. With the rise of suburban life, expanding payroll systems, and the growth of commercial banking, checks became the backbone of everyday transactions. By the 1980s and 1990s, Americans were writing tens of billions of checks per year, more than any other country in the world. Even today, the United States remains one of the last major economies where checks still play a significant role in business and government payments.

Several factors explain this longevity: a deeply rooted financial culture, slow modernization of banking infrastructure, and the legal framework established by the Uniform Commercial Code (UCC), which standardized check processing nationwide. While many countries shifted rapidly to electronic transfers, the U.S. maintained a hybrid system where checks continued to thrive.

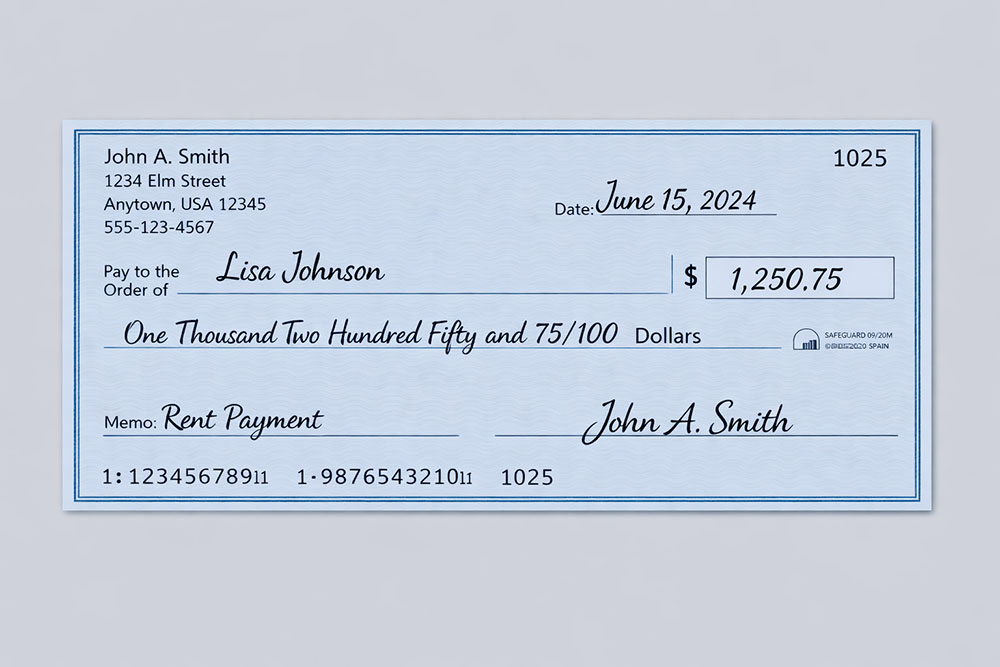

How to Properly Write a Traditional Paper Check

Despite the rise of digital payments, millions of Americans still write checks every day. Filling one out correctly is essential, because a mistake can invalidate the payment or even expose the writer to fraud. Here are the key steps and techniques:

- Date line — Write the full date in month‑day‑year format. Post‑dating (writing a future date) is allowed but not always honored by banks.

- Payee line — Clearly write the name of the person or business receiving the money. Any ambiguity can cause delays or disputes.

- Amount in numbers — Write the exact amount, including cents, using digits. Start at the far left to prevent tampering.

- Amount in words — Spell out the amount in English. This line legally overrides the numeric amount if the two differ.

- Memo line — Optional, but useful for noting rent, invoice numbers, or tax‑related details.

- Signature line — Sign your name exactly as it appears on your bank account. Without a signature, the check is invalid.

These steps may seem simple, but they reflect a system built on handwritten authorization and physical verification—features that feel increasingly outdated in a digital world.

The Shift Toward Electronic Checks

As technology advanced, the U.S. banking system introduced the electronic check (e‑check), a digital version of the traditional paper check. Instead of handwriting information, the payer authorizes a transfer electronically, and the bank processes it through the Automated Clearing House (ACH) network.

E‑checks preserve the legal structure of traditional checks but eliminate the need for paper, postage, and manual handling. Businesses embraced them quickly because they reduce processing time and cost. Government agencies also use e‑checks for tax refunds, benefits, and vendor payments.

Still, the transition has been gradual. Many small businesses, landlords, and older consumers continue to rely on paper checks out of habit, trust, or convenience. The U.S. financial system, unlike Europe’s SEPA or the U.K.’s Faster Payments, has not fully standardized instant transfers across all banks, which slows the decline of checks.

When Will Paper Checks Disappear?

Predicting the end of paper checks in the United States requires balancing cultural, technological, and regulatory factors. The trend is clear: check usage has been declining by 8–12% per year for more than a decade. Younger generations rarely use them, and businesses increasingly prefer digital invoicing and automated payments.

A realistic forecast is that:

- Paper checks will lose mainstream relevance by the early 2030s

- They may survive in niche uses—legal settlements, insurance claims, and certain business payments—until around 2040

- Full elimination will depend on universal adoption of real‑time payments and regulatory pressure, neither of which is guaranteed in the short term

In other words, checks are not disappearing tomorrow, but their long reign is undeniably nearing its end.

Where the Paper Check Goes From Here

The American paper check is a fascinating blend of tradition and practicality. It shaped the country’s financial habits for more than a century, survived multiple technological revolutions, and still plays a role in modern commerce. Yet its future is limited. As digital payments become faster, safer, and more universal, the paper check will gradually fade into history—remembered as a symbol of an earlier era of American banking.